All That Glitters is not Gold

October 20, 2025

By Matt Andera

By Matt Andera

Securities AnalystYou’ve likely heard the phrase “all that glitters is not gold.” But in the case of precious metals this year, gold (and silver for that matter) are shining brightly. Gold is up over 60% this year and has more than doubled since the beginning of 2024. In fact, gold has outpaced the S&P 500 and Dow Jones Industrial Average since the year 2000. Impressive returns for an asset that is generally considered to be a safe haven in times of volatility. Driving the rapid rise in price has been inflation concerns, geopolitical uncertainty, de-dollarization fears, and central bank purchasing. Given the recent performance and media attention, we’ve received some questions about gold as an investment. Two commonly cited reasons to invest in gold are to hedge against inflation and to offer downside protection. Let’s explore these claims further.

Inflation Hedge

One of the most important reasons to invest is to ensure that we maintain purchasing power. Inflation in moderate levels is a sign of a healthy, growing economy. However, over time the effects diminish the spending power of money. By investing, we can ideally earn a rate of return that is above the rate of inflation to maintain our purchasing power. How does gold compare to something like stocks to achieve this? As I mentioned earlier, gold has certainly excelled over the past 25 years. The annualized return of gold since 2000 has been 11%, compared to the S&P 500 at 8%. But things look a little different when you zoom out further. Over the past 50 years, gold has returned 6.4% annually compared to the 12.5% annualized return of the S&P 500. While recent performance of gold compared to stocks has been favorable, stocks have significantly outperformed over a longer time period and provided better inflation-adjusted returns.

Downside Protection

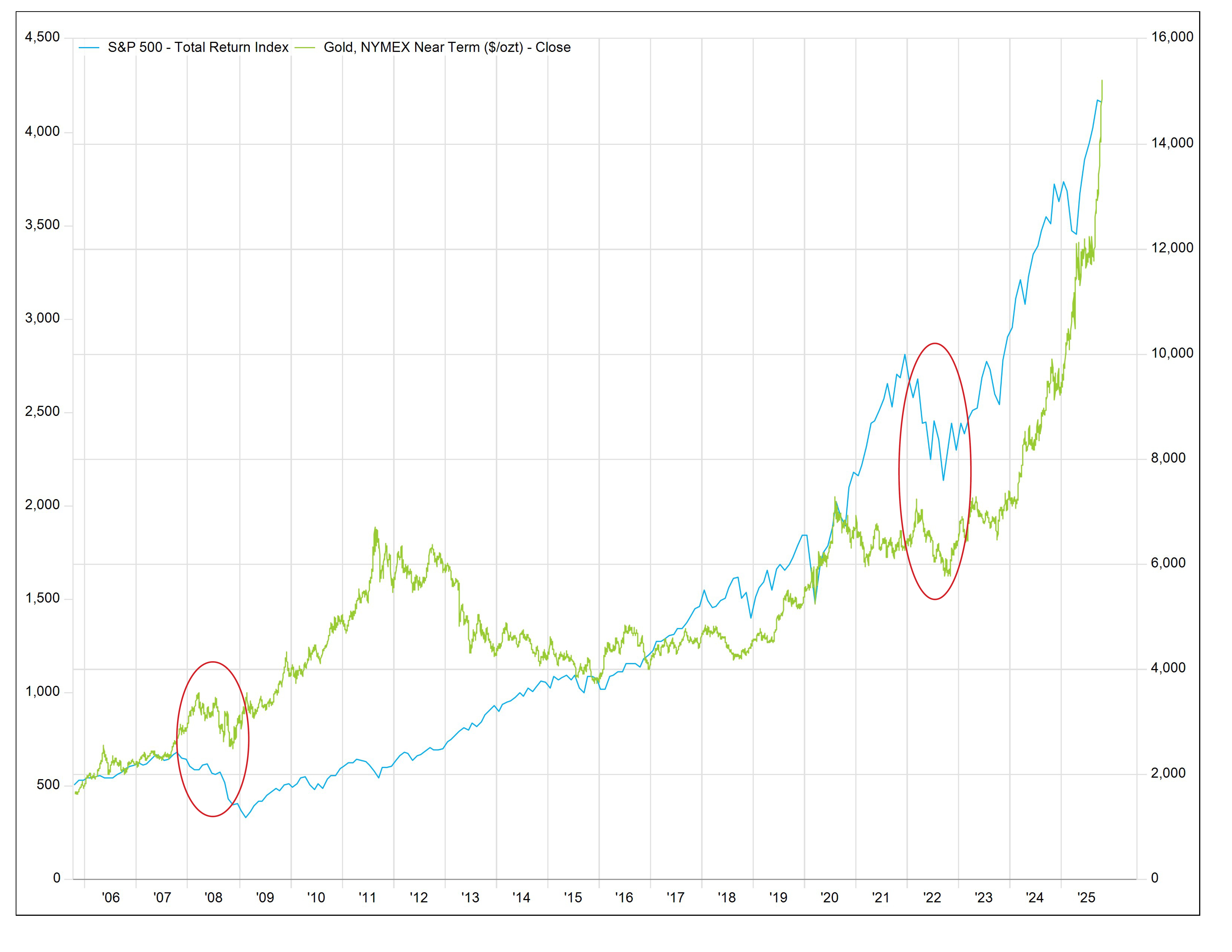

Gold is generally considered to be a safe haven and offer protection in turbulent markets. While gold investors were protected from the tariff-related market sell off in April, that is not always the case in bear markets. Looking back to other recent periods of volatility such as 2008 and 2022, gold counterintuitively saw price declines alongside equities. This can be seen in the chart below tracking the S&P 500 (in blue) and gold prices (in green) over the past 20 years, with those volatile periods circled in red.

Additionally, the price of gold has actually been more volatile than the S&P 500 over the same time period.

While gold can certainly play a role in a well-diversified portfolio, history suggests that equity markets provide better inflation-adjusted returns. And with a diversified fixed income portfolio yielding over 4.5%, we can secure protection with lower volatility while still realizing positive inflation-adjusted returns. While gold has its moments of brilliance, successful investing requires looking beyond the recent shine. To further discuss how we structure portfolios to meet your long term goals, please reach out to an advisor. Your financial success matters to us.